Table of contents

Introduction

Every year, individuals, businesses, and associations in Pakistan face the crucial responsibility of filing their income tax returns. With the deadline set at September 30th, it’s imperative to understand the process, the consequences of missing the deadline, and the benefits of timely filing.

The Legal Framework: Income Tax Ordinance, 2001

The Income Tax Ordinance, of 2001, serves as the primary legal document governing the taxation system in Pakistan. It outlines the obligations, penalties, and procedures related to income tax return filing.

Why is Income Tax Return Filing Important?

Maintaining Transparency

It provides a clear record of your earnings, deductions, and taxes paid, as emphasized in Section 114.

Facilitating Financial Transactions

For loan approvals, visa applications, or business contracts, a consistent tax filing record is often required, as mentioned in Section 116.

Claiming Refunds

If you’ve paid more tax than you owe, filing returns is the only way to claim a refund, as per Section 170.

Consequences of Missing the Deadline

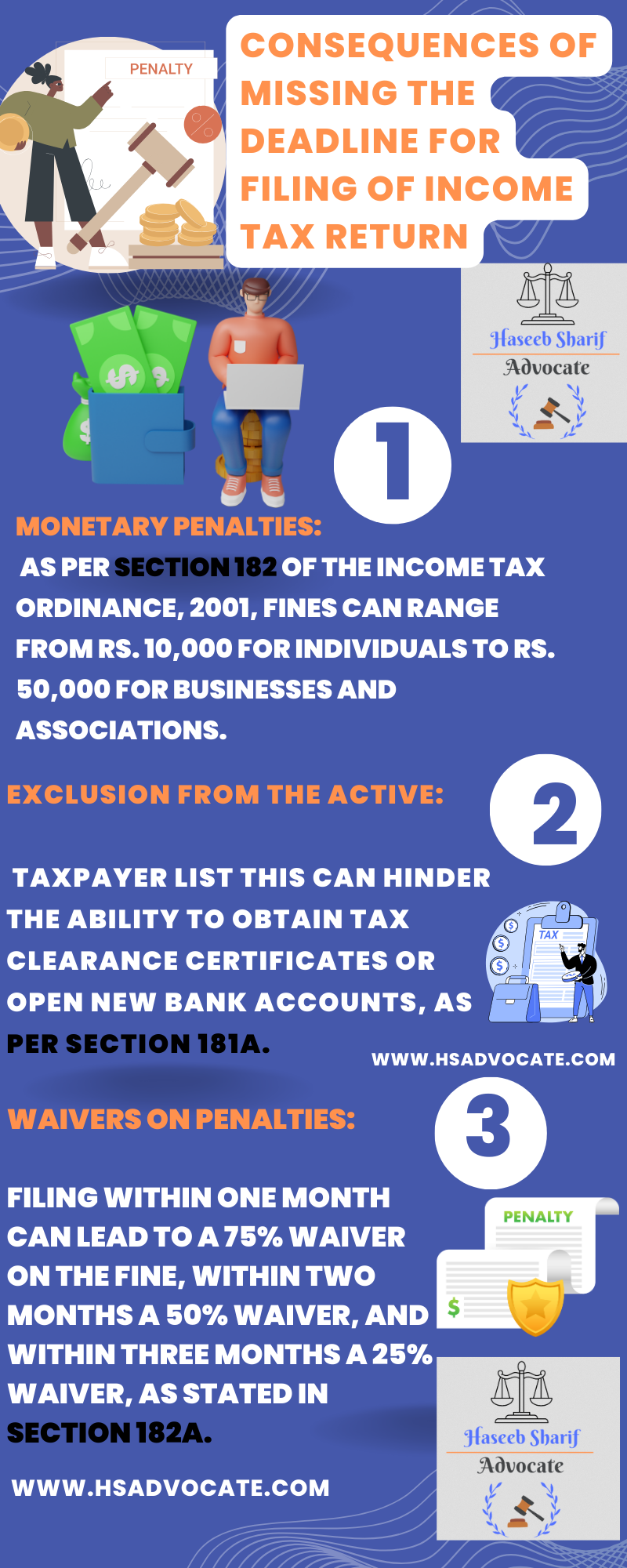

Monetary Penalties

As per Section 182 of the Income Tax Ordinance, 2001, fines can range from Rs. 10,000 for individuals to Rs. 50,000 for businesses and associations.

Waivers on Penalties

Filing within one month can lead to a 75% waiver on the fine, within two months a 50% waiver, and within three months a 25% waiver, as stated in Section 182A.

Exclusion from the Active Taxpayer List

This can hinder the ability to obtain tax clearance certificates or open new bank accounts, as per Section 181A.

Tips for Smooth Filing

Stay Updated

Regularly check the official Federal Board of Revenue website for any changes in forms or regulations.

Organize Documents

Keep all relevant financial documents handy for a hassle-free filing process.

Seek Professional Help

If unsure about the process, consider hiring a tax consultant or using online platforms.

Income Tax Rates and Slabs for Rental Income, 2022-2023

Advanced Taxation: Wealth Statement and Reconciliation

As per Section 116, taxpayers may also be required to file a wealth statement and its reconciliation, detailing assets and liabilities.

FAQs

The deadline is September 30th each year. Now for the tax year 2023 last date of filing is 31st October.

Missing the deadline can result in monetary penalties and exclusion from the Active Taxpayer List.

Yes, but it might come with penalties depending on the delay.

You can log into the official FBR portal to check the status of your submission.

Yes, several online platforms and apps can guide you through the process.

Conclusion

While income tax return filing might seem daunting, understanding its importance and being prepared can make the process smoother. It’s not just about fulfilling a legal obligation but also about contributing to the nation’s growth and ensuring personal financial transparency.